OFFER OPT-IN

Project Brief

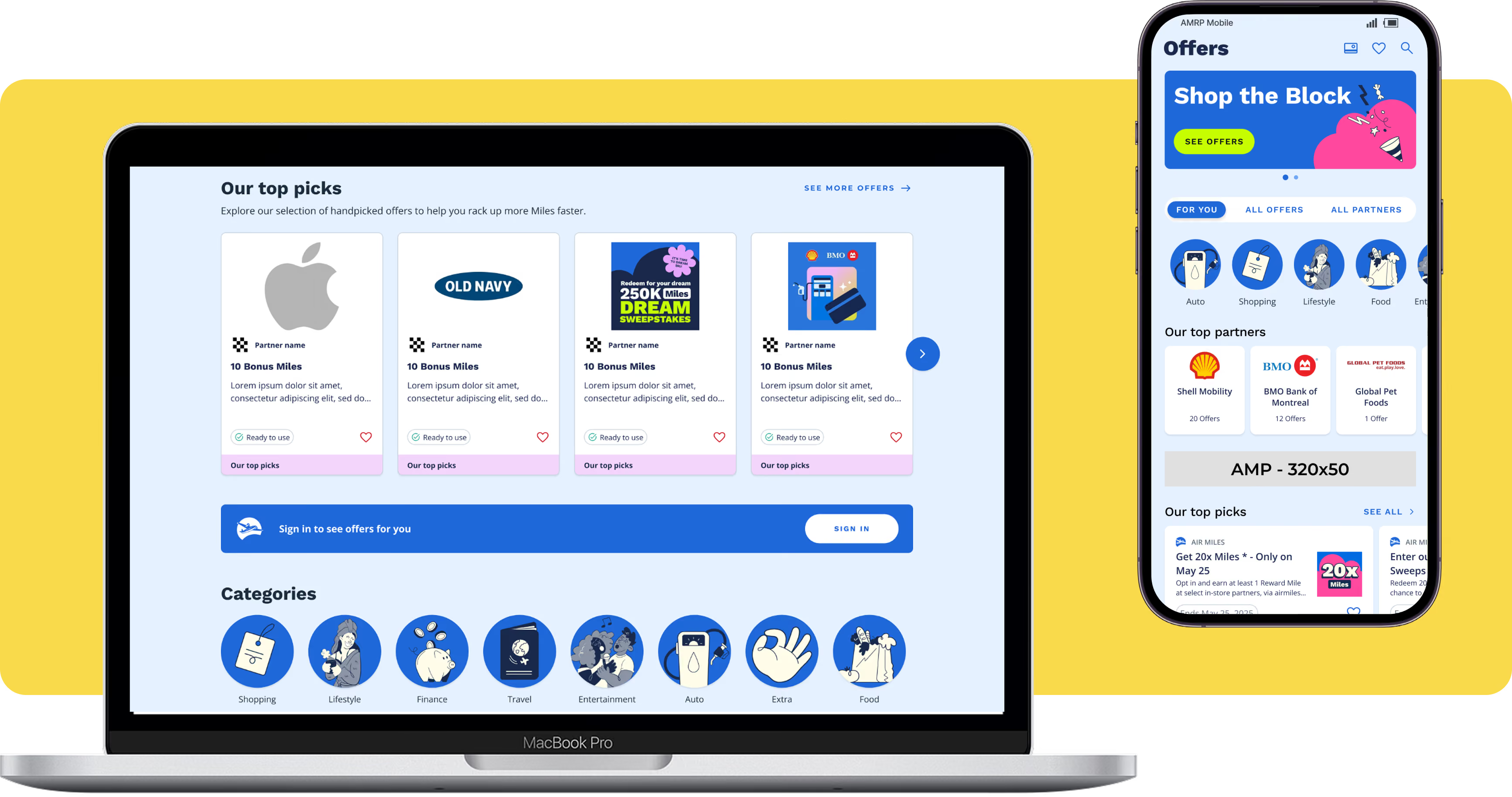

Card Linked Offers let collectors earn Miles without any extra steps at checkout. By linking a Mastercard to their account, a collector unlocks new partners and earning opportunities whenever they pay with that card.

In late 2025, Air Miles expanded this offering by automatically linking 2.4 million known BMO Debit Card holders. This created a problem for partners, who pay for every Mile issued: they wanted assurance that cardholders were intentionally choosing to earn with them, not passively accumulating Miles. They began requiring explicit opt-in on each offer as a condition of partnership.

The Challenge

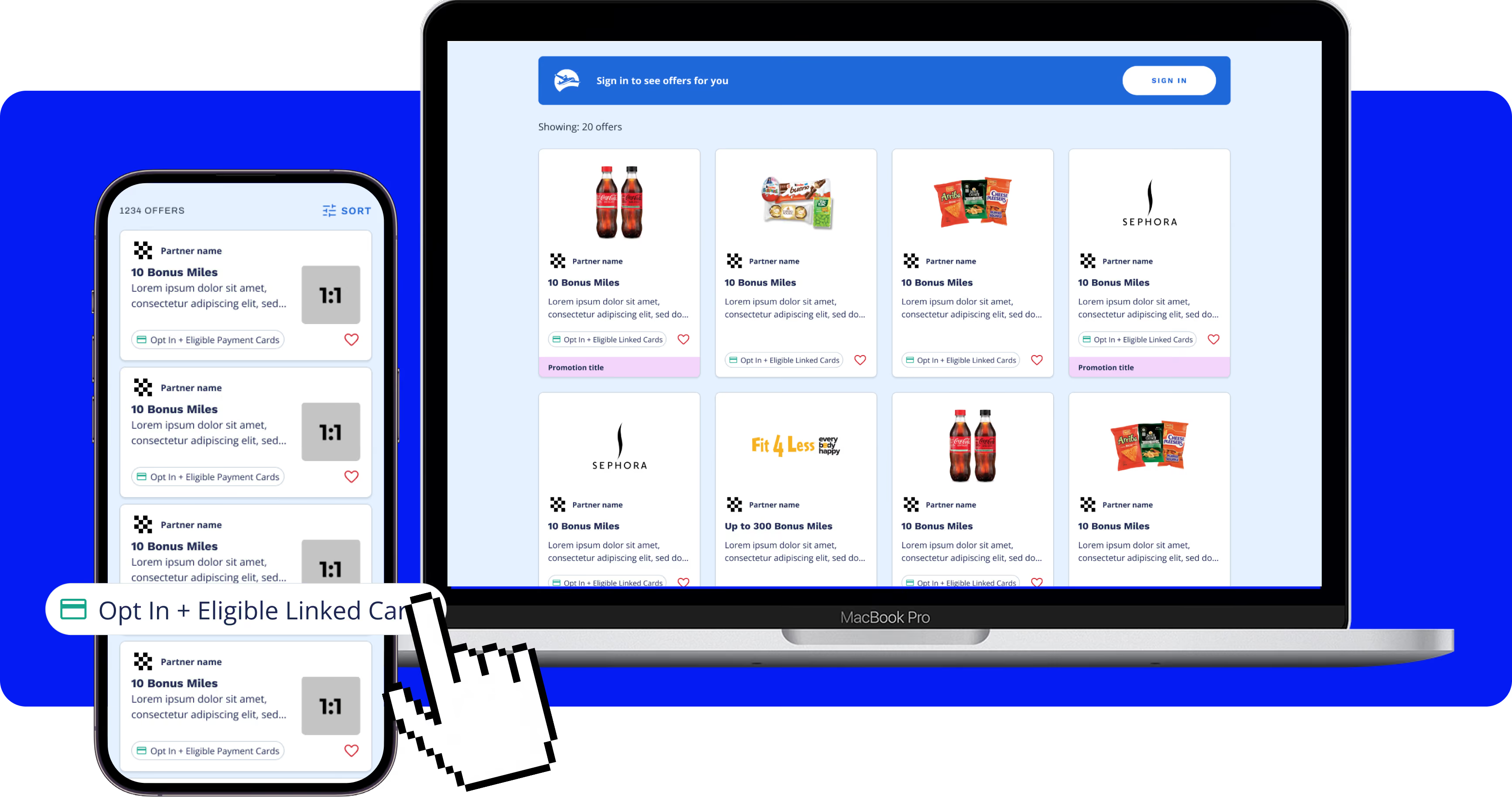

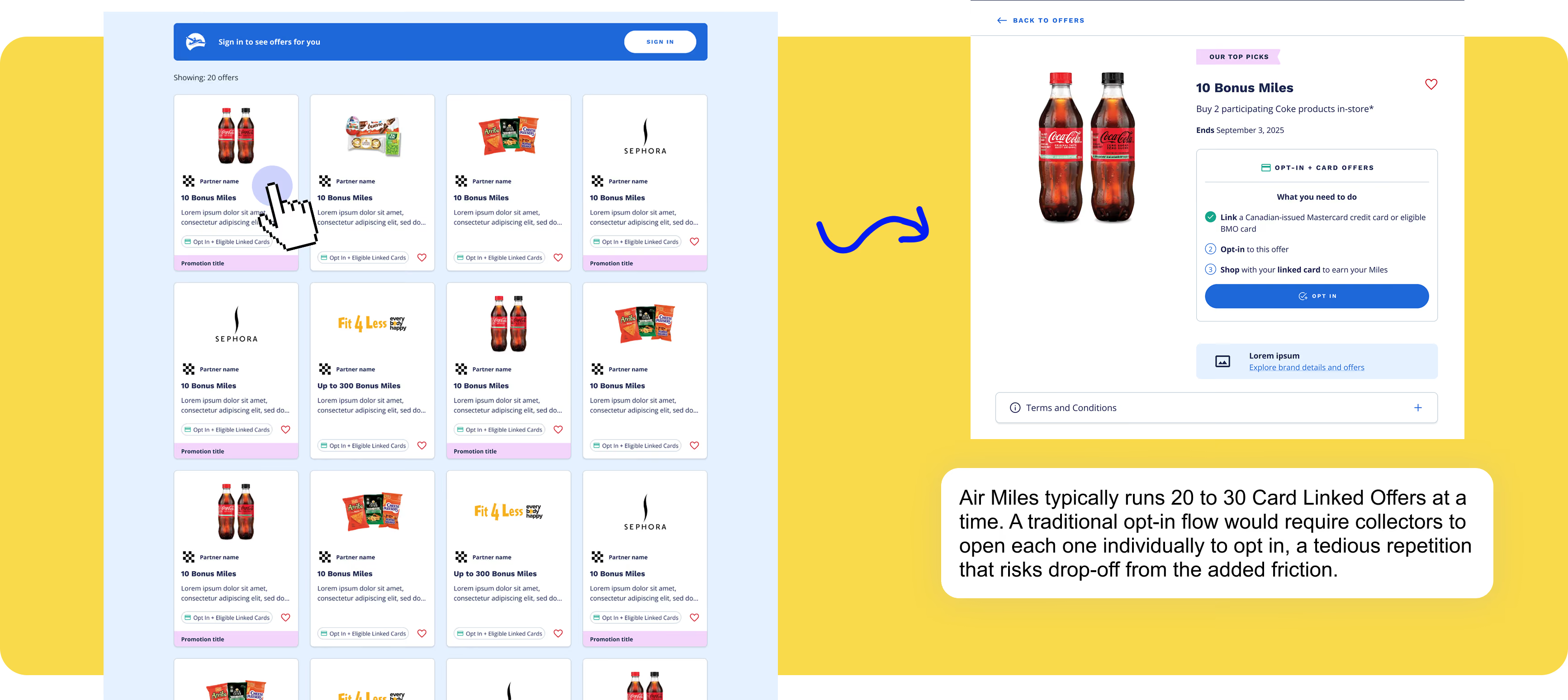

A traditional opt-in model would require collectors to open and opt into each offer individually, an unreasonable task on a page with a minimum of 20 live offers at once.

Without single-offer opt-in, our organization was losing $50,000 in monthly revenue from partners who wouldn't sign on or reseign without it. The number itself was modest, but many partners start with Card Linked Offers to test the program before committing to larger contracts. Losing them meant losing not just that monthly revenue, but also the potential of bigger deals down the line.

Research & Discovery

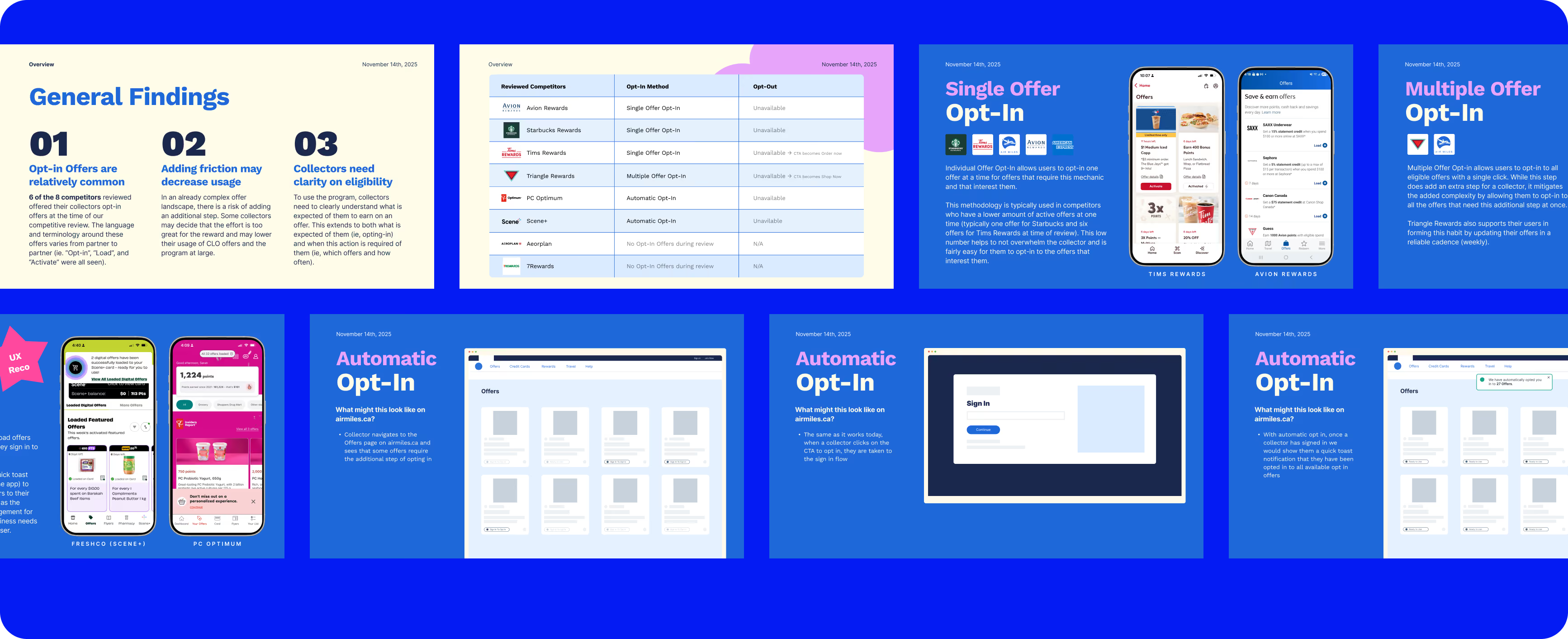

A review across competiting loyalty programs revealed three opt-in models: single-offer opt-in (collectors opt in individually per offer), multi-offer opt-in (one action opts in all offers), and automatic opt-in (offers activate on sign-in).

I presented these options to Strategic Partnership stakeholders and recommended automatic opt-in as the least disruptive path for collectors. Partners disagreed, arguing it didn't demonstrate enough conscious intent.

After several design iterations that either added complexity or strayed from partner requirements, I turned to our data for clarity on how collectors actually engage with offers. I reviewed roughly 30 collector session recordings on Fullstory to see exactly how users interacted with offer cards, and found a pattern: whenever a card displayed an "Opt-In" mechanic pill, collectors clicked directly on the pill instead of the rest of the card, even though it wasn't interactive. I found this behaviour to be unique to opt-in offers. Collectors were already showing their intent to opt in, directly from the card.

To validate whether this behaviour extended to Card Linked Offers specifically, I set up a targeted filter to view sessions focused on our one existing Card Linked Opt-In offer with Sephora. The behaviour was consistent.

The answer wasn't a new design pattern. It was following how our collectors were naturally behaving.

The Design Approach

The behavioural insight pointed to a simple solution: follow the collectors' actions and let them opt in by interacting with the mechanic pill itself.

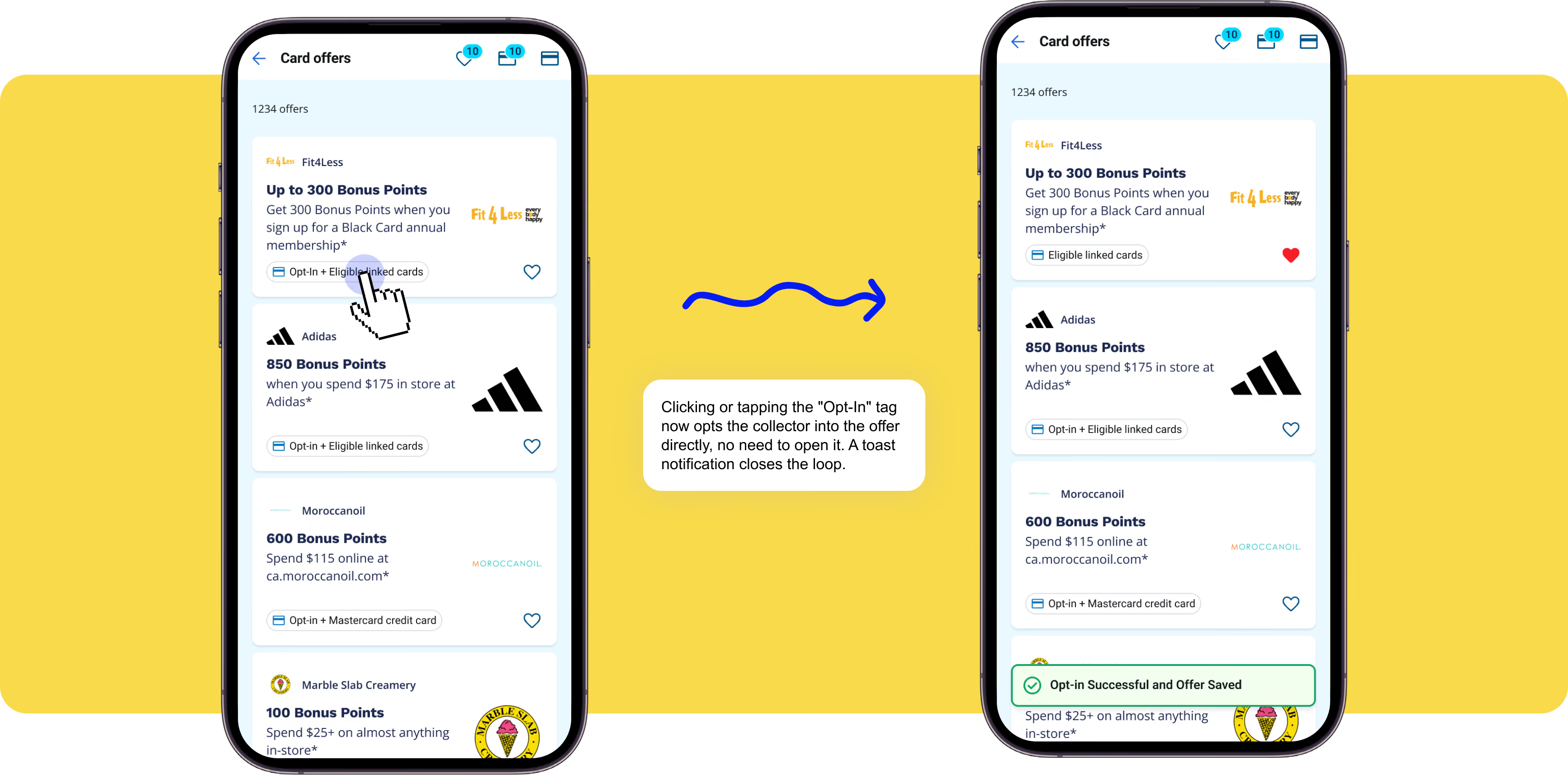

In the new designs, when a collector taps the pill, they're opted into the offer. The pill state updates from "Opt-In + Eligible Linked Cards" to "Eligible Linked Cards," and a toast notification confirms the action, closing the loop. This keeps the experience simple for collectors while measuring intent more precisely.

The Outcome

By understanding existing collector behaviour, I arrived at a solution that satisfied partner requirements without adding a single extra step for collectors. Partners aligned on the approach and accepted it as sufficient demonstration of intent.

The opt-in mechanic required no new components, a far smaller technical lift than building a net-new opt-in flow would have required. Digging into the data revealed a solution that satisfied collector expectations, evolving business requirements, and technical constraints, all without adding bloat, tech debt, or friction to the flow.